China’s economy has continued to grow rapidly since the mid-1990s, and the demand and output of basic metals such as copper, aluminum, lead and zinc have also been continuously and rapidly increased. The smelting technology of these basic metals has also been changing with each passing day. For example, advanced oxygen-enriched bath smelting technology has been popularized in most copper and lead smelting enterprises in China, hydro-zinc smelting technology is continuously upgraded and developed in China's zinc smelters, the electrolytic aluminum technology with China's independent intellectual property rights has developed rapidly, reaching the international leading level in many aspects. With technological progress, national policies also strongly support enterprises to improve resource utilization efficiency. Therefore, the environmental protection level and comprehensive utilization of resources in China's non-ferrous metal industry have significantly improved. At the beginning of this century, China's production of electrolytic aluminum, electrolytic copper, primary lead, and refined zinc all reached the world’s largest production, accounting for more than 40% of global production. At the same time, the minor metals, associated with these basic metals, such as cadmium, indium, bismuth, germanium, gallium, selenium and tellurium, their output also ranks among the top in the world.

However, China is still a developing country and is in a critical period of industrialization. It also has the insufficient development problem of the high-tech, new materials and emerging industries. The decrease of the products consumption lead to an oversupply of most minor metals and they have to export a large quantities. While exporting a large number of primary products, it has to import a large number of high-tech products such as ITO targets, gallium arsenide and indium phophide. In the field of basic metals, China turned into a major importing country from a major exporting country. A large amount of import and export trade promotes exchanges and cooperation between China and the world. The highly mature international market objectively requires the accelerated development of China's non-ferrous metal marketization.

Since 1998, China has actively promoted the development of the domestic futures market. From then to 2015, major non-ferrous metals such as copper, aluminum, lead, zinc, nickel, tin, gold and silver were all listed and traded on the Shanghai Futures Exchange. However, minor metal has always lacked a standardized market in China, especially the lack of authoritative price guidelines. Therefore, in order to promote the prosperity and standardized development of China's minor metal market, Fanya Metals Exchange (hereinafter refer to Fanya) , which uses minor metals such as indium, antimony, and tungsten as the main trading targets, was established in 2012. In 2015, Fanya was closed, 14 kinds of strategic metals of indium, germanium, ammonium paratungstate (APT) , bismuth, gallium, and silver approximately 198,547 tons of products were seized. Four years later, the various stocks of Fanya were auctioned from October to December 2019, with a total bid amount of about 8.4 billion yuan (about 1.2 billion US dollars).

After the closure of Fanya, China comprehensively implemented supply-side structural reforms, strengthened environmental protection, and cleared excess production capacity in all industries. Meanwhile, Sino-US trade frictions have intensified, and global economic uncertainty has further strengthened. The resonance of the macro environment at home and abroad has led to the sluggish demand in the entire non-ferrous metal market, the problem of overcapacity has become prominent, and the price of minor metals such as indium has continued to fall, in 2017, it entered the cost zone.

The low-price operation for more than 3 years has hit the supply of these minor metals to a considerable extent. The US's full suppression of China has stimulated the localization of China's high-tech industries. The domestic demand for some minor metals such as indium, gallium and germanium has shown a good growth momentum. Although covid-19 epidemic has affected the demand since 2020, but the overall trend shows it is still growing. After more than 20 years of hard work, a large number of application technologies in China have basically matured. Many industries have proposed that swift actions must be taken to address problems, plug loopholes, and reinforce weak links, prime resources should be focused and strategic planning made to deal with "key areas and stranglehold problems" and then make breakthroughs at the earliest possible date in these fields. The deterioration of the international trade environment will promote China's downstream industries to actively use domestically produced technologies and materials, thereby accelerating the process of replacing imports, promoting domestic consumption, and supporting economic internal circulation. In this way, we believe that China's direct consumption of minor metals will compose a new canto. Optimistic expectations for future demand may be an important reason for the smooth auction of Fanya stocks.

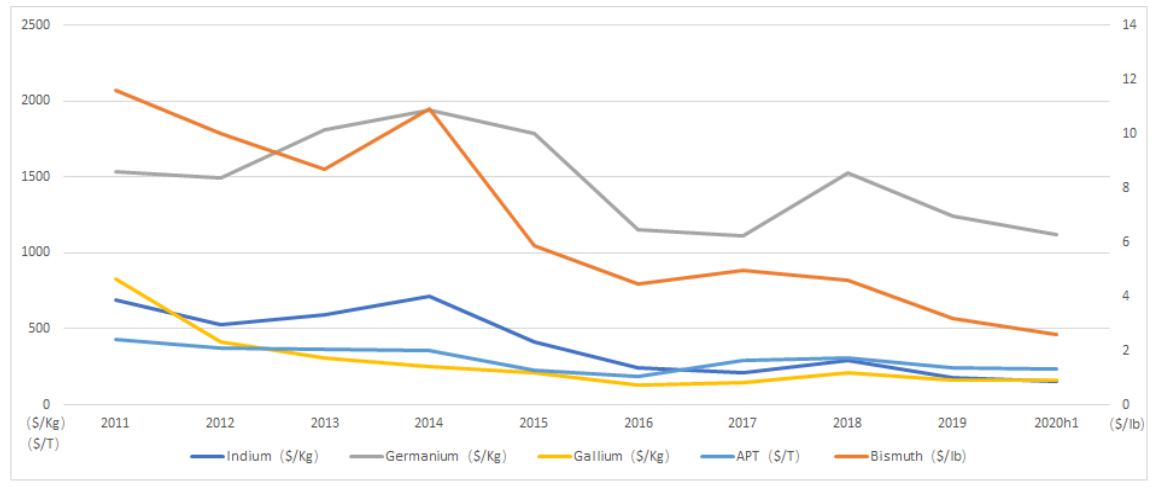

At the end of 2019, after the auctions of the Fanya stocks, the prices of related minor metal didn't see sharp fallen. On the contrary, some varieties' prices even rebounded significantly due to good demand. Take indium, bismuth, germanium, gallium, tellurium, APT as examples, the price of indium was US$160/kg before the auction, 2020H1 average price was 3.75% lower than pre-auction; the price of bismuth was US$2.75/lb before the auction, 2020H1 average price was 4.3% lower than pre-auction; the price of germanium was US$1175/kg before the auction, 2020H1 average price was 4.8% lower than per-auction; the price of gallium was US$157.5/kg before the auction, 2020H1 average price was 1.1% higher than per-auction; the price of tellurium was US$45/kg before the auction, 2020H1 average price was 20% higher than per-auction; the price of APT was $200/ton, 2020H1 average price was 16.5% higher than pre-auction.

Since Fanya stocks auction, the supply and demand status of the above six varieties in the Chinese market is as follows:

Indium: 3,609 tons Fanya refined indium stocks, equivalent to about two years of global demand, are putting considerable pressure on the market. Covid-19 has a certain impact on indium consumption from March to May, and it has improved in the past two months. But the indium market sentiment is more pessimistic in the first half of 2020, the domestic price has been fluctuating below 1,000 yuan/kg. In the long term, the demand for indium in China's display and semiconductor industries is still in a stage of rapid growth, and major demand companies such as BOE continue to increase their consumption of domestic targets. Vital Materials Co., Limited, the acquirer of Fanya indium stocks, has become China's largest ITO target producer. The stocks may be in order to meet its own production needs in the future and ensure that there will be no shortage of indium in 3-5 years. From the perspective of supply capacity, the future growth of China's lead-zinc mines will be finite, and the indium grade of resources will be depleted. It is expected that the production of primary refined indium has entered a plateau, and the future growth space is already finite, and indium recovery needs to be strengthened.

Indium: 3,609 tons Fanya refined indium stocks, equivalent to about two years of global demand, are putting considerable pressure on the market. Covid-19 has a certain impact on indium consumption from March to May, and it has improved in the past two months. But the indium market sentiment is more pessimistic in the first half of 2020, the domestic price has been fluctuating below 1,000 yuan/kg. In the long term, the demand for indium in China's display and semiconductor industries is still in a stage of rapid growth, and major demand companies such as BOE continue to increase their consumption of domestic targets. Vital Materials Co., Limited, the acquirer of Fanya indium stocks, has become China's largest ITO target producer. The stocks may be in order to meet its own production needs in the future and ensure that there will be no shortage of indium in 3-5 years. From the perspective of supply capacity, the future growth of China's lead-zinc mines will be finite, and the indium grade of resources will be depleted. It is expected that the production of primary refined indium has entered a plateau, and the future growth space is already finite, and indium recovery needs to be strengthened.

Bismuth: After the Fanya 19,228 tons bismuth stocks were sold at the end of 2019, the Bismuth price hovered around $2.6/lb for a long time, nearly 30% above the winning bid of $2.04/lb. The domestic price has dropped from 60,000 yuan/ton to below 40,000 yuan/ton. The stock is equivalent to more than a year’s global consumption. It is expected that the market demand will be moderate in the next few years. In 2020, due to the impact of the global epidemic, demand is unlikely to improve in the short term. However, in the long term, depressed prices are conducive to demand growth, as is expected in industries such as pharmaceutical, solder, and alloys. From the supply side, low price led to the change of supply structure in China. Major bismuth producers were hit hard by the last round of steep price plummets. At present, copper and lead smelting companies have become the main supply forces for bismuth, copper, and lead enterprises will be based on price conditions to moderately control the sale of bismuth. The bismuth stocks controller will not suffer losses in the future and will also control the inventory release rhythm.

It is estimated that 19,228 tons of Fanya bismuth stocks will be slowly digested for at least five years, and the impact on bismuth prices will be within a controllable range, but the low-price range is inevitable.

Germanium: At present, the germanium price has been already close to the production cost, even fell to below the cost in a time, so that there is no more space for further decline. Fanya germanium stocks are equivalent to China's annual output, posing less threat to the market. Moreover, for Vital, the successful bidder of Fanya germanium stocks, a complete industrial chain of germanium has been formed, transformed from a primary product producer to a major supplier of processed products. Germanium stock is an import material guarantee for Vital. China's germanium production is highly concentrated, the industrial chain continues to improve, and product quality continues to improve. Great progress has been made in quality certification for downstream users. The prospects for domestic and foreign demand are good. Under the leadership of high-end demand, China's germanium industry is moving towards. It is the future trend to set production by sales. Therefore, it is expected that germanium prices will fluctuate within a reasonable range in the future.

Gallium: China is the world's leading producer of gallium, accounting for more than 90% of global production. 191 tons Fanya gallium stock is equivalent to nearly half of China's annual production. China's ability to become a major gallium producer in the world is mainly due to the high content of gallium in Chinese bauxite. In recent years, the shortage of domestically produced bauxite in China has forced the production of gallium to halt. Companies bidding for Fanya stocks saw a bottom price for gallium and an upward trend in gallium production costs in the future. Therefore, the auction process is extremely fierce, and the mark up range is much higher than other varieties. In addition, several gallium consumption areas including 5G, compound semiconductors, chips, etc., are expected to become the next explosive point for the growth of gallium consumption demand. With the relatively stable consumption of LED as support, China's gallium market is full of confidence. For Vital, the successful bidder, it is a direct consumer of gallium and has no own resources. Therefore, the Fanya gallium stocks acquired will be used as a company's self-sufficient resource for long-term. Although some gallium stocks are flowing to the market to ease the financial pressure of enterprises. However, under the situation of supply has been cut off in half in China, a small amount of Fanya stocks outflow has very limited impact on the market.

Tellurium: Tellurium is mainly used for photovoltaic and temperature difference refrigeration. Fanya announced tellurium stock is 170 tons, about a quarter of global annual consumption. But after the auction, the price rose instead of falling. The reason is that, as a by-product of copper, the production of tellurium continues to be stable, while consumption is increasing year by year with the fierce demand for cadmium telluride photovoltaic products. At present, cadmium telluride is in a leading position in the competition of various photovoltaic thin film products, and its shipment volume is significantly higher than that of other types of thin film solar products. At the same time, apart from the United States, China is already becoming the world's second largest producer of cadmium telluride products. The production capacity of China's cadmium telluride photovoltaic materials and products is actively expanding. Therefore, for the tellurium market, the Fanya tellurium stocks which accounts for only a quarter of the annual consumption, will not pose a threat to the market, maybe just to meet consumption growth in the next 2-3 years.

Tellurium: Tellurium is mainly used for photovoltaic and temperature difference refrigeration. Fanya announced tellurium stock is 170 tons, about a quarter of global annual consumption. But after the auction, the price rose instead of falling. The reason is that, as a by-product of copper, the production of tellurium continues to be stable, while consumption is increasing year by year with the fierce demand for cadmium telluride photovoltaic products. At present, cadmium telluride is in a leading position in the competition of various photovoltaic thin film products, and its shipment volume is significantly higher than that of other types of thin film solar products. At the same time, apart from the United States, China is already becoming the world's second largest producer of cadmium telluride products. The production capacity of China's cadmium telluride photovoltaic materials and products is actively expanding. Therefore, for the tellurium market, the Fanya tellurium stocks which accounts for only a quarter of the annual consumption, will not pose a threat to the market, maybe just to meet consumption growth in the next 2-3 years.

Ammonium Paratungstate (APT): Tungsten is one of China's superior rare resources, and China's supply of tungsten products accounts for more than 80% of the global market share. China’s annual output of APT is 120,000 tons, and Fanya stocks accounts for 23.67% of domestic annual output. If it is directly put into the market, it will have a greater impact on prices. However, due to its important strategic value, Chinese tungsten suppliers attach great importance to tungsten resources, and the auction transaction price of Fanya APT stock is higher than the market price at that time. Meanwhile, the winning bidder, China Molybdenum Co., Ltd., will reserve Fanya APT stock as future tungsten raw material and it will not flow to the market in a short time, so it will not have a direct impact on the price.

Nearly one year has passed since the Fanya stock auction ended, and the market reacted differently to different types of inventory. In 2020, due to covid-19, most downstream consumer markets for non-ferrous metal products will be affected to varying degrees. Chinese governments at all levels in China are also actively formulating various policies to help companies and industries overcome difficulties. For example, the Yunnan Provincial Government is promoting commercial purchasing and storage, which will greatly facilitate the stable operation of some minor metal varieties market. In general, the impact of the Fanya stocks on the market will continue for some time, but the pressure is less than before the auction. Through the digestion in the next 2-4 years, the impact of these stocks will eventually disappear. Perhaps China's demand expectations and market sentiment will reverse.

Mai Liu - Senior Manager - Minor Metals & Rare Earth, Beijing Antaike Information Co., Ltd. & Vice Secretary General- InBi-Ge & Ga-Se-Te Branch, CNIA

Xu Sun - Indium, Antimony, Tellurium Senior AnalystŁ¬Antaike & Vice Secretary General - Antimony BranchŁ¬CNIA

Zhaohui Yang - Tungsten Senior Analyst

Yilan Li - Germanium, Gallium Senior Analyst